Think of mobile detailing business insurance as a specialized toolkit of policies, each one designed to protect you from the unique financial risks you face on the job. It’s not just a “nice-to-have” item on your checklist; it’s the bedrock of your business, safeguarding your gear, your reputation, and your personal finances. Without it, one bad day could easily shut you down for good.

Why Mobile Detailing Insurance Is Your First Line of Defense

Picture this: you’re applying the finishing touches to a mirror-like ceramic coat on a client's brand-new SUV. Out of nowhere, a gust of wind topples your buffer stand, and it clatters right onto the hood, leaving a deep, ugly scratch. That single, unfortunate moment could cost you thousands in repairs and, worse, torpedo the reputation you’ve worked so hard to build.

This is exactly why insurance isn't just another business expense—it's what lets you sleep at night. It turns a potential financial disaster into a manageable problem.

The Real-World Risks You Face Daily

Every single job is different. Unlike a detailer working in a controlled shop, you're out in the wild, navigating driveways, parking garages, and curbsides. The environment is constantly changing, and that's where the biggest risks lie.

Here are just a few common scenarios where insurance becomes your best friend:

- Accidental Vehicle Damage: It happens. You might scratch a fender with a buckle, short out an electrical system with a pressure washer, or use a chemical that reacts poorly with a delicate surface.

- Third-Party Property Damage: Think beyond the car itself. Maybe you get overspray on a client’s freshly painted garage door or crack a patio stone with your water tank.

- Client or Visitor Injury: A customer could easily trip over your power cord or slip on a patch of wet pavement you just created, leading to a nasty fall, medical bills, and a potential lawsuit.

- Equipment Theft or Damage: Your van is a treasure chest of expensive tools. Polishers, extractors, and steamers can be stolen in a heartbeat or damaged as you travel between jobs.

A solid mobile detailing insurance policy is your financial shield. It’s the one thing that ensures a simple mistake doesn't drain your bank account or force you to hang up your polisher for good. For anyone just starting out, this protection is absolutely non-negotiable.

Building Credibility and Trust

Having the right insurance does more than just protect you—it proves you’re a professional. It tells clients that you're serious about your business and that you stand behind your work.

In fact, many high-end clients, apartment complexes, and fleet managers won't even talk to you unless you can provide a Certificate of Insurance (COI). This is a standard requirement for many service professionals, and you can learn more about essential business insurance for contractors to see how it applies across the industry.

Ultimately, being properly insured doesn’t just keep you safe; it opens doors to bigger, better-paying jobs. As you map out your business, taking stock of your entire mobile car wash setup will help you pinpoint exactly what risks you need to cover.

Understanding Your Core Insurance Coverage

Think of your mobile detailing insurance not as a single, one-size-fits-all policy, but as a custom-built toolkit. Each type of coverage is a specialized tool designed to handle a very specific—and potentially very expensive—problem. If you don't have the right tools in your kit, you're leaving your business wide open to risk.

Let's break down the essential policies that form the foundation of protection for any serious mobile detailer. Getting a solid grip on what each one does is the first step toward building a business that can weather any storm.

General Liability: The Foundation Of Your Protection

This is the bedrock of your entire insurance plan. General Liability Insurance is your shield against claims that your business operations caused bodily injury or property damage to someone else—basically, anyone who isn't you or an employee. It’s designed for accidents that happen around the vehicle you're working on, not to the vehicle itself.

Imagine a client walking out to check on your progress and tripping over your pressure washer hose. They sprain their ankle and need a trip to the emergency room. Or, picture a scenario where overspray from a cleaning chemical drifts onto their prized rose bushes, killing them. General Liability steps in to cover the medical bills, legal defense costs, and any potential settlements from these types of incidents.

A simple slip-and-fall accident on a client's property could easily generate a claim averaging over $30,000. Without General Liability, an everyday mishap could become a financial catastrophe for your business.

Garagekeepers Liability: Your Client Vehicle Shield

While General Liability protects the client's property around the car, Garagekeepers Liability is built specifically to protect the vehicle you're actually working on. This coverage is absolutely critical for detailers, as it covers damage to a customer's car while it's in your "care, custody, or control."

This is the policy that kicks in for the most common detailing-related mishaps. Did you accidentally burn through the clear coat with a new polisher? Short out an electronic component with a bit of water? What if someone vandalizes the car while it's parked at a job site under your supervision? Garagekeepers Liability is designed to pay for those repairs.

Simply put, it addresses the single biggest risk of your profession: working directly on someone else's expensive and valuable asset.

Inland Marine: Your Equipment Bodyguard

Your equipment is the lifeblood of your mobile operation. That pressure washer, extractor, polisher, and steamer represent a huge investment, and they're always on the move, which makes them incredibly vulnerable. Inland Marine Insurance acts as a personal bodyguard for your tools and equipment while they are in transit or sitting at a job site.

This policy protects your gear from common threats like:

- Theft: Someone breaks into your van overnight and steals your high-end detailing setup.

- Damage: Your gear gets mangled in a car accident while you're driving between appointments.

- Fire or Vandalism: Your equipment is destroyed while stored at a temporary location.

Standard business property insurance usually only covers items at a fixed address. Since your business is mobile by nature, Inland Marine fills that crucial gap. It ensures you can quickly replace your essential tools and get back to work without a massive out-of-pocket expense.

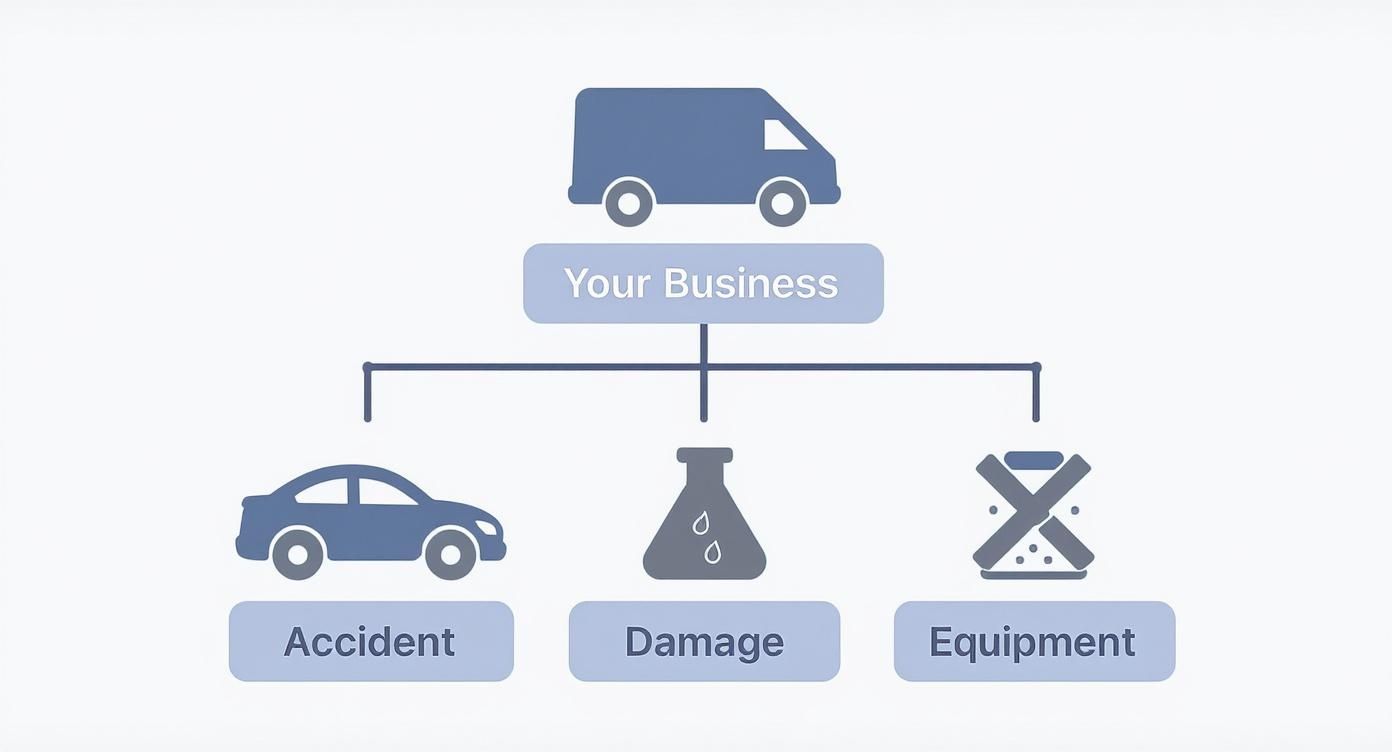

This infographic really helps visualize how your mobile business faces these distinct risks every single day—accidents, property damage, and equipment loss—and why each one needs its own specific type of insurance.

To help you keep these straight, here's a quick rundown of the essential coverages we've talked about.

Essential Insurance Policies for Mobile Detailers

| Policy Type | What It Protects | Real-World Example |

|---|---|---|

| General Liability | Third-party bodily injury or property damage claims. | A client trips over your power cord, breaks their wrist, and sues you for medical bills. |

| Garagekeepers | Damage to a customer's vehicle while it's in your care. | You accidentally burn through the paint with a polisher, requiring a panel to be repainted. |

| Inland Marine | Your tools and equipment while in transit or at a job site. | Your van is broken into, and your $5,000 worth of detailing equipment is stolen. |

| Commercial Auto | Liability and physical damage for your work vehicle. | You cause an accident while driving between client appointments, and your personal policy denies the claim. |

These core policies work together to create a safety net, allowing you to focus on growing your business instead of worrying about what could go wrong.

The Critical Role Of Commercial Auto Insurance

Finally, let's talk about the vehicle you drive for work. It's a common mistake, but a personal auto insurance policy almost always excludes coverage for accidents that happen while you are conducting business. Just driving to a client's house, transporting your equipment, or even having your business logo on your van can be enough for a personal insurer to deny a claim.

This is why Commercial Auto Insurance is completely non-negotiable. It provides much higher liability limits and is specifically designed to cover your vehicle for business use, protecting you from accidents on the road. Understanding the crucial difference between commercial vs personal auto insurance is fundamental for any mobile detailer. Ignoring this distinction can lead to devastating financial consequences after an accident.

What Happens When Your Detailing Business Starts to Grow?

When your detailing business shifts gears from a weekend side-hustle to a full-time operation with a growing team, your risks change in a big way. The basic insurance that covered you as a one-person show just won't cut it anymore. Scaling up means adding new, more specific layers of mobile detailing business insurance to protect yourself against bigger and more complicated problems.

It’s a lot like upgrading your detailing equipment. You probably started with a simple, off-the-shelf polisher. But as you started tackling tougher paint corrections and more clients, you invested in a professional-grade, dual-action machine. Your insurance needs to follow that same path, getting stronger and more capable as your business grows.

Covering Your Crew and Vehicles on the Move

Your work van is your office on wheels, but the minute you hire employees, your risks on the road multiply. This is where you can't afford to skimp on specialized auto coverage.

We've already talked about Commercial Auto Insurance as the baseline for any vehicle used for business. But as you add people to your team, another policy becomes absolutely essential: Hired & Non-Owned Auto (HNOA) Insurance.

This is the policy that kicks in when your employees use vehicles you don't actually own to do company business. Say you send an employee to pick up supplies in their own Toyota Camry and they cause an accident. HNOA is designed to cover the liability costs that go beyond what their personal auto policy will pay. Without it, your business could be on the hook for the damages.

The Must-Have Insurance for Your Employees

The day you hire your very first employee—even if it's just a part-time helper for busy weekends—you enter a whole new world of legal responsibilities. The biggest one is Workers' Compensation Insurance. In fact, it's required by law for employers in nearly every single state.

Workers' comp is there to protect both you and your team. If an employee gets hurt on the job, this policy helps pay for:

- Medical Bills: From the initial ER visit to follow-up physical therapy.

- Lost Wages: It replaces a chunk of their income while they're recovering and can't work.

- Rehab Costs: Helps them get the treatment they need to return to work safely.

Think about it: an employee could easily throw out their back lifting a pressure washer or get a chemical burn from a new degreaser. Workers' comp ensures they get the medical care they need without having to sue you. This protects their well-being and saves your business from a lawsuit that could sink you.

Don't ever mess around with this one. Skipping legally required Workers' Compensation can lead to crippling fines, state-issued stop-work orders, and in some cases, even criminal charges. It’s not just a good idea—it’s the law.

Protecting Your Business in a Digital World

Even a hands-on business like auto detailing runs on data. You're storing customer names, phone numbers, addresses, and maybe even credit card info in your scheduling software or on a laptop. That information is valuable, and it's your job to keep it safe.

That’s what Cyber Liability Insurance is for. This coverage is built to help you bounce back after a data breach or cyberattack.

If a hacker gets into your system and steals your client list, Cyber Liability can help cover the expensive aftermath, including:

- The cost of notifying every customer who was affected.

- Paying for credit monitoring services to protect them from identity theft.

- Hiring a PR firm to help manage your reputation.

- Covering legal fees and regulatory fines that come with a breach.

As your business and client list grow, so does your digital risk. This policy ensures a problem on your computer doesn't destroy the real-world business you've worked so hard to build. Each of these coverages acts as another piece of armor, making sure your detailing business is ready for the challenges that come with success.

How Much Does Detailing Insurance Really Cost?

Let's get right to it—the number one question on every detailer's mind: what is this actually going to set me back? It's easy to see insurance as just another bill, but that's the wrong way to look at it. Think of it as an investment in your company's survival and your own peace of mind.

The price you'll pay for mobile detailing insurance isn't some random number. It's calculated based on your specific business and the risks you face every day. While there's no one-size-fits-all price tag, most new, solo mobile detailers can find a solid policy that won't break the bank.

Sure, as your business grows, your premium will likely grow with it. But that cost will always be a tiny fraction of what you'd pay out-of-pocket for a single, major claim.

What Factors Influence Your Insurance Premium?

Insurance companies are all about managing risk. They look at a bunch of different factors to figure out how likely you are to file a claim. The more risk they see, the higher your premium will be. Understanding what they're looking for helps you make sense of the quotes you receive.

Here are the main things that will shape your cost:

- Your Location: Working in a busy, high-traffic city is usually more expensive than detailing in a quiet suburb. The odds of theft, vandalism, and traffic accidents are simply higher.

- Services You Offer: A simple wash-and-wax job has very little risk. But if you’re doing high-end paint correction or applying ceramic coatings, a small mistake can lead to a repair bill that costs thousands.

- Value of Your Equipment: The more your gear is worth, the more it costs to cover it. Insuring a $10,000 setup with an Inland Marine policy is naturally going to cost more than covering a $2,000 starter kit.

- Your Claims History: If you have a clean record with no past claims, insurers see you as a safe bet. That almost always translates to better rates.

Think of it like this: Your policy limit is the max payout from your insurer for a covered claim. A $1 million per occurrence limit means they'll pay up to that amount for a single incident. A $2 million aggregate limit is the total they'll pay for all claims during your policy year. This structure protects you from one massive disaster and a string of smaller mishaps.

Understanding Typical Cost Ranges

While every quote is different, it helps to have a ballpark figure in mind for budgeting. Carrying insurance is now standard practice, with industry data showing that over 75% of professional mobile detailers are covered.

For most small to mid-sized operations, the average annual premium for mobile detailing business insurance in the U.S. typically falls somewhere between $1,200 and $3,500. You can find more insights into the U.S. car wash and auto detailing industry to see how the market is growing.

That price usually gets you a Business Owner's Policy (BOP) that bundles the essentials, like General Liability and Garagekeepers Liability.

What pushes you toward the higher end of that range? Things like having employees, operating several work vans, or specializing in high-end exotic and luxury cars. A solo operator with a modest equipment list will land on the lower end, making professional protection affordable right from the start.

Finding and Securing the Right Insurance Policy

Shopping for mobile detailing insurance doesn't have to be a headache. If you do a little prep work upfront, you can navigate the process with confidence and land a policy that’s a perfect fit for your business. It's a lot like detailing itself—the final result is only as good as the prep work you put in.

A smooth quoting process starts with having all your ducks in a row. An insurance agent can dial in a much more accurate and speedy quote when you come to the table prepared with the specifics of your operation.

Your Pre-Quote Information Checklist

Before you start calling agents or filling out online forms, pull together these key details. Taking a few minutes to do this now will save you a ton of time later and make sure the quotes you get actually reflect what you need.

- Business Structure Details: Have your official business name, address, and Employer Identification Number (EIN) ready. If you're a sole proprietor, your Social Security Number will work.

- List of Services: Be specific. Write down everything you do, from a basic wash-and-wax to multi-step paint correction and ceramic coatings. Different services carry different risks.

- Annual Revenue Estimates: Have a good handle on your projected or current annual gross sales. Insurers use this to understand the size and scope of your business.

- Equipment and Tool Inventory: Make a list of your big-ticket items—pressure washer, steam cleaner, polishers, generator—and what it would cost to replace them today.

- Vehicle Information: For any van, truck, or trailer you use for work, you'll need the year, make, model, and VIN.

Finding the Right Agent and Comparing Quotes

Here’s a pro tip: not all insurance agents are the same. You need someone who gets the auto service industry. Look for brokers who specialize in commercial auto or artisan contractor policies, as they’ll already know the ins and outs of coverages like Garagekeepers.

Once you have a few quotes in hand, it's time to compare them. And please, don't just look at the monthly price. A cheap policy with major coverage gaps is one of the most expensive mistakes you can make.

When you lay policies side-by-side, sweat the details. Pay close attention to the policy limits, the deductibles, and especially the exclusions. That lower premium might look great until you see it comes with a $2,500 deductible you'd have to pay out-of-pocket after an accident.

Asking the Right Questions Before You Sign

Before you sign on the dotted line, you need to ask a few pointed questions. This is your chance to make sure there are no nasty surprises waiting for you when you actually need to use your insurance.

- Does this policy include Garagekeepers Liability? Get a clear "yes" and make sure you understand the coverage limits.

- Is my equipment covered while I'm driving and while I'm working at a customer's house? This confirms your Inland Marine coverage is set up correctly.

- What does the claims process look like? A company that's easy to work with when things go wrong is worth its weight in gold.

- How do I get a Certificate of Insurance (COI)? You'll need this proof of insurance to work with commercial clients or in some upscale neighborhoods.

Following these steps makes you an informed buyer, not just another customer. Building a business the right way involves many pieces, and for those just starting out, we've created a complete guide on how to start a detailing business that dives into more than just insurance. Locking in the right policy is a huge step toward building a professional, resilient, and trustworthy company.

Smart Risk Management That Lowers Your Premiums

Let's be honest: the best insurance claim is the one you never have to file. While a solid mobile detailing business insurance policy is your safety net, actively managing your risks on every job is the single best way to keep your long-term costs down. Insurance carriers love businesses that take safety seriously, and they show it by offering better premiums.

Think of yourself from an insurer's point of view. A detailer with a clean claims history is a much safer bet than someone who’s constantly reporting minor accidents. By putting professional safety protocols in place, you’re not just avoiding expensive mistakes—you’re building a track record that makes insurance companies want to work with you. It’s a proactive approach that cements your reputation as a true professional who doesn’t leave things to chance.

Creating Your Safety Playbook

A strong safety culture starts with documenting your process. It doesn't have to be complicated. In fact, it's the small, consistent actions that prevent the most common mishaps, whether it's a chemical spill on leather or an accidental scratch from a pressure washer. A simple, repeatable system is your best shield.

Here are a few practical habits you can build into your workflow right away:

- Mandatory Vehicle Inspections: Before you even unroll a hose, do a complete walk-around of the client's vehicle. Use a checklist on your phone or tablet to note every pre-existing ding, scratch, or electronic quirk. Snap photos from all angles to create a clear "before" picture.

- Rigorous Chemical Handling: Don't just "wing it" with your chemicals. Create strict rules for how they are used, stored, and transported. Make sure every bottle is clearly labeled and that everyone on your team knows the right product and technique for every surface.

- Secure Your Work Zone: Use cones or caution tape to clearly define your work area. This simple step keeps kids, pets, and curious neighbors from tripping over your equipment and protects the client's car from accidental bumps.

"A proven track record of safety is your most valuable asset when negotiating insurance rates. Every job completed without incident strengthens your case for a lower premium, proving you are a low-risk, high-quality operator."

Documentation Is Your Best Defense

Getting into the habit of meticulous record-keeping is more than just good organization—it's one of your most powerful risk management tools. When you maintain detailed files for every job, you create a factual record that can shut down bogus claims or disputes before they even start.

Your job file for each client should include:

- The pre-service inspection form and all your "before" photos.

- A signed service agreement that clearly states what you're going to do.

- Any notes about special client requests or unusual vehicle conditions.

- A set of "after" photos showing the pristine, finished work.

This level of detail gets noticed by both customers and insurance underwriters. It demonstrates that you run a tight ship, which is a massive factor in getting better insurance rates. The global auto detailing business insurance market has swelled to around USD 2.68 billion, partly because the risks are getting more complex with new vehicle technology and advanced detailing chemicals. Insurers are actively looking for professional operators who know how to manage those risks. You can see how the insurance market is adapting to industry growth to better understand this trend.

Ultimately, managing risk and using the right equipment are two sides of the same coin. Check out our comprehensive mobile detailing equipment list to make sure you have the right tools. When you combine professional-grade gear with a professional-grade safety mindset, you’re setting your business up for long-term, profitable success.

Your Top Detailing Insurance Questions, Answered

Jumping into the world of business insurance can feel a bit overwhelming, and it's natural to have questions. Let's tackle some of the most common ones we hear from mobile detailers just like you.

Can I Just Use My Personal Auto Insurance for My Work Van?

This is a huge one, and the answer is a hard no. It’s probably the riskiest mistake a new detailer can make. Your personal auto policy is written with a specific exclusion for business use, which means if you get into an accident while driving to a job, your insurer has every right to deny the claim flat out.

Even just having your logo on your van can be enough for them to consider it a commercial vehicle. You absolutely need a proper Commercial Auto Insurance policy to cover your work van. It's designed to protect you when you're on the clock.

Think of it this way: using personal auto insurance for your business is like bringing a garden hose to a house fire. It’s simply not the right tool for the job, and the financial consequences of a denied claim could be devastating.

I Only Detail on Weekends. Do I Still Need Insurance?

Definitely. The risk of accidentally scratching a client’s car, dropping a buffer on their garage floor, or having a pressure washer hose trip someone doesn't magically go away if you're working part-time. An accident can happen whether you're detailing your first car or your five-hundredth.

The good news is that insurance costs are tied to your exposure. Carriers look at your revenue and how many cars you service, so a part-time gig will naturally have a much lower premium than a full-time, multi-employee operation. The protection, however, is just as crucial.

A Commercial Client Asked for Proof of Insurance. What Do I Give Them?

They're asking for a Certificate of Insurance, often just called a COI. This is a standard, one-page document that acts as a snapshot of your coverage. It shows what policies you have, your liability limits, and the dates your coverage is active.

Getting one is a breeze. Just call or email your insurance agent, and they can usually send a PDF over the same day, almost always for free. Having a COI ready to go makes you look professional and is non-negotiable for landing those lucrative commercial and fleet jobs.

Ready to give your vehicle a professional-level clean without the hassle? The SwiftJet Car Wash Foam Gun turns any garden hose into a powerful foaming system, making car care faster and more effective. Discover the difference and get your SwiftJet today!